Thank you!

Oops! Something went wrong while submitting the form.

Cancel

.png)

Gaming’s Moneyball Moment

Nexon’s December 2011 IPO was the second largest in the world that year, and over the course of a three-week roadshow, my team and I met with fund managers and analysts at many of the world’s largest institutional investors. The meetings were rigorous and remarkably consistent. Most believed they already understood the games business. They had invested in companies like EA, Activision, and Square-Enix, and their mental model was clear: games launch, revenue peaks, and then declines. Growth comes from replacing old hits with new ones. R&D is inherently risky.

Nexon did not fit that model. Our business was not built around game launches, but virtual worlds designed to last and grow for many years. We had been private for seventeen years and could show long histories of sustained growth in online games like MapleStory and Dungeon & Fighter.

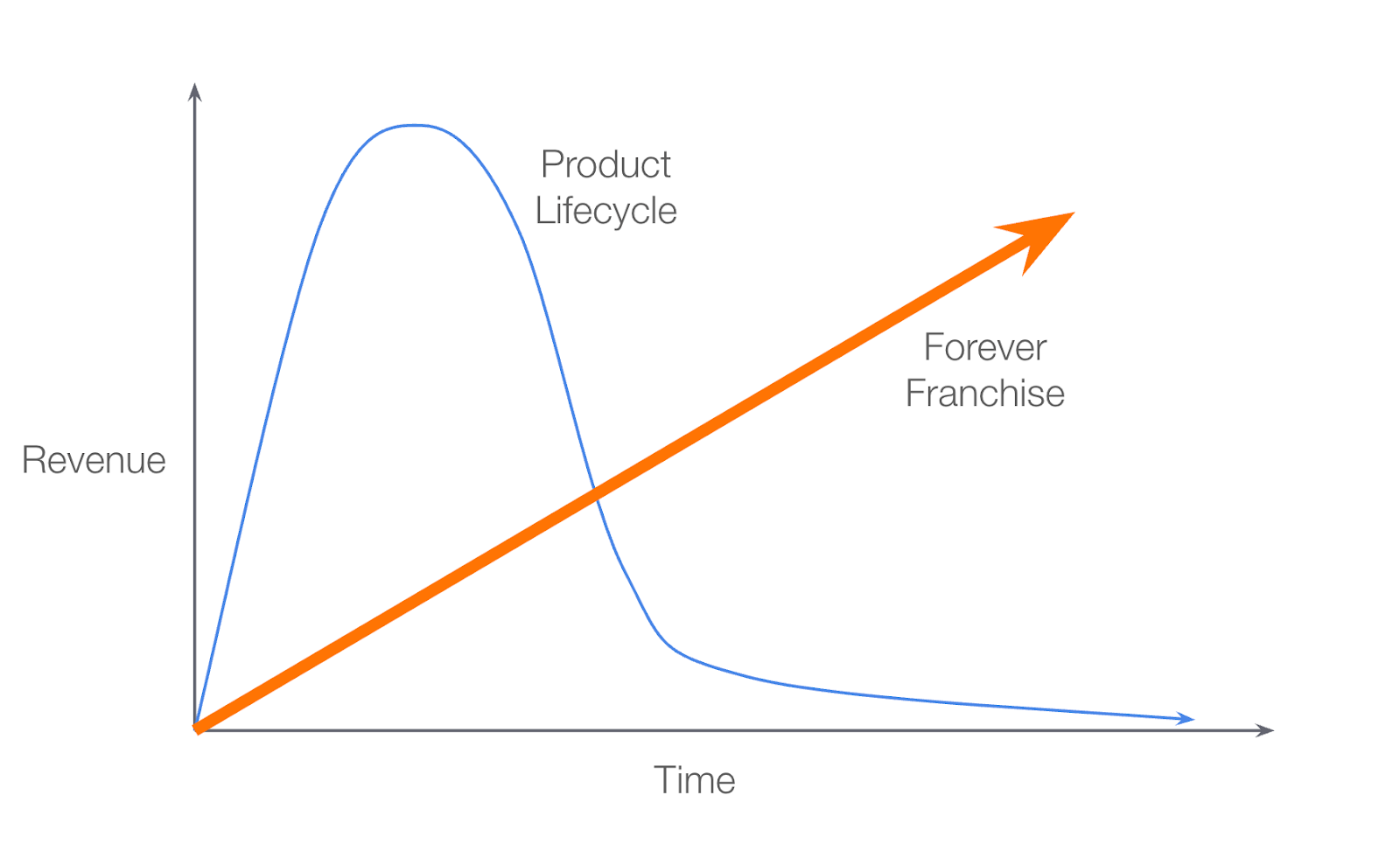

We showed this graphic on the first page of our roadshow deck:

The reaction ranged from skepticism to hostility. Some investors were polite, asking when our games (represented by the orange line) would finally decline. Others were blunt, insisting that the industry simply did not work the way we described. Our data contradicted an assumption so deeply ingrained that few recognized it as an assumption at all, and many were unwilling to abandon it even when confronted with evidence.

A decade and a half later, those same games are many times larger than they were at the IPO, having grown at double-digit rates for years on end. Today Nexon is a giant.

Yet the underlying confusion remains. The idea that a videogame can last for decades is widely understood in theory, but routinely abandoned in practice.

This essay makes a simple claim. The industry broadly understands that some games can last and grow for a long time; what it consistently gets wrong is how to act on that belief. Under pressure, teams and investors revert to finite-game instincts precisely when persistence and disciplined reinvestment matter most. The result is a systematic undervaluation of durable franchises and a repeated abandonment of compounding opportunities. This misunderstanding is rooted in a mental model that no longer describes how the best games behave.

For decades, the industry has been analyzed using a Product Lifecycle mental model: games launch, revenue spikes, and then decays. Most investors still evaluate videogame businesses using near-term revenue growth as a proxy for health. The underlying assumption is rarely stated: once a game peaks, it is on its way out.

But that assumption is often wrong. The most fragile online businesses often look strongest in the near term, while the healthiest ones pass through periods of flat or declining revenue. In the best games, revenue often declines precisely when long-term value is rapidly rising.

The most valuable games in the world – The Forever Franchises – are operated as long-lived worlds: not launched and replaced, but designed to retain players over time and evolve continuously. Sustained fun – as measured by player retention and other fundamental metrics – not launch revenue, determines their economic destiny.

This creates a structural mismatch between perception and reality. Companies that are quietly compounding value through retention and system health in their live games are dismissed as stagnant or broken. Games that extract revenue aggressively in the near term are rewarded, even as their underlying player bases erode.

Once you internalize that inversion — and are willing to act on it consistently under pressure — much of the industry’s behavior stops making sense. Monetization strategies, organizational structures, greenlight processes, and executive incentives are revealed to be downstream of a single false assumption.

The Forever Franchise is not a new idea. It has existed in plain sight for more than two decades. What remains rare is the willingness to fully abandon the old mental model and act on a more accurate one. Like Moneyball, it’s a story about the courage to trust a better model before the results are proven to everyone.

If Product Lifecycle is your view of the world, several implications are obviously downstream:

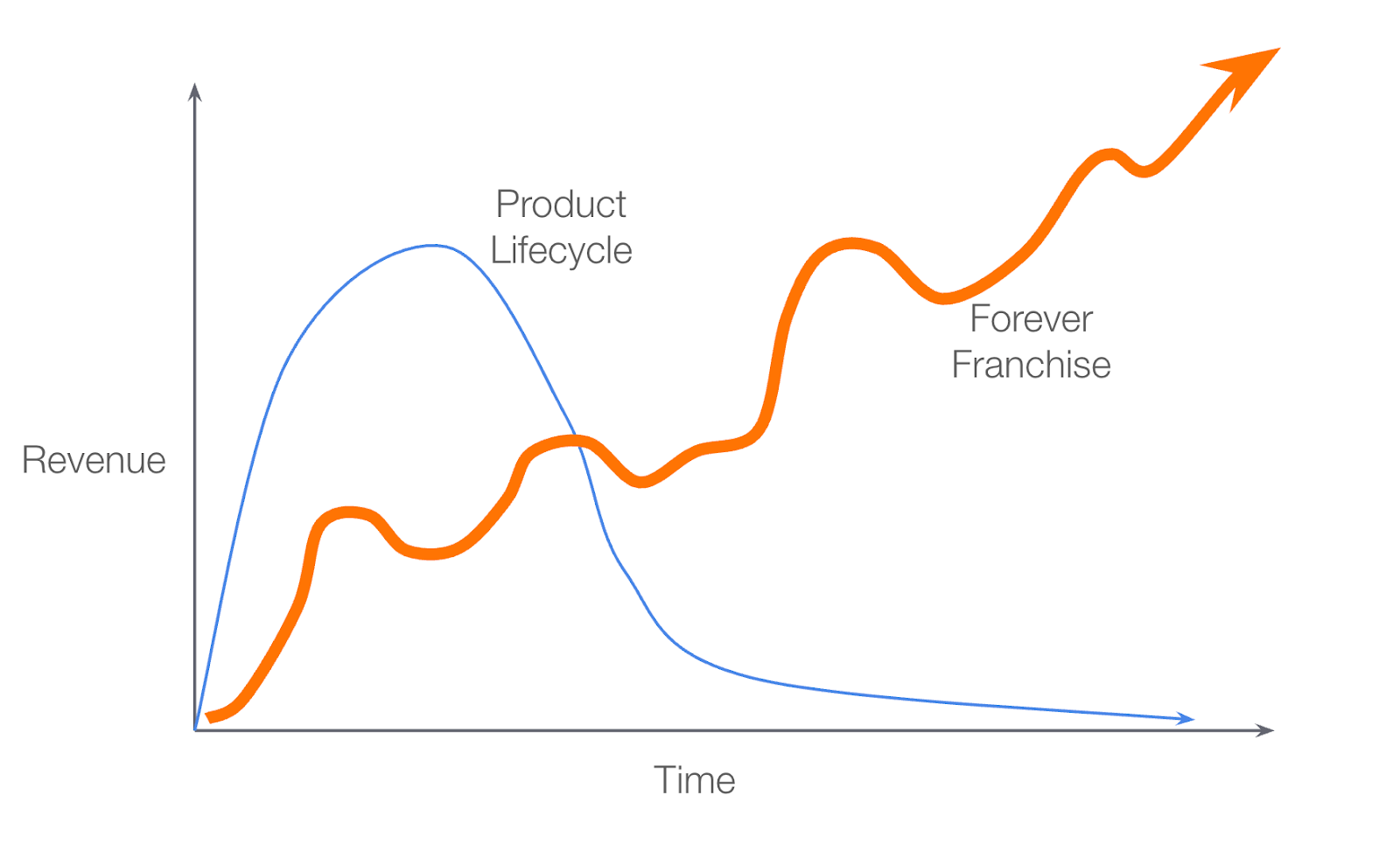

Within that dominant mental model, a small number of games proved to be extraordinarily long-lived, confounding analysts who were operating from a Product Lifecycle view. These included games from Korea such as MapleStory and Dungeon & Fighter, as well as Western titles like Warframe and DotA 2.

If you think the orange line is how a game should work – that this is even possible – you’ll start thinking differently about how you organize your business:

There are many valid approaches to monetization, each with real trade-offs. Those choices are largely downstream of a single belief: that a game can last and grow for years or decades. Everything else follows from that.

Let’s get a little more precise. The growth of a successful live game is never a straight line. It moves up and down in the near term as the game evolves.

Live games are updated continuously. Some updates are small fixes or tuning changes, others are major additions to the game world. Not all of them succeed. Some introduce bugs or balance issues that temporarily harm the experience and drive players away. In well-run games, those mistakes are identified and corrected, and the community returns. Short-term volatility is not a sign of failure. It is the normal operating pattern of a healthy, evolving system.

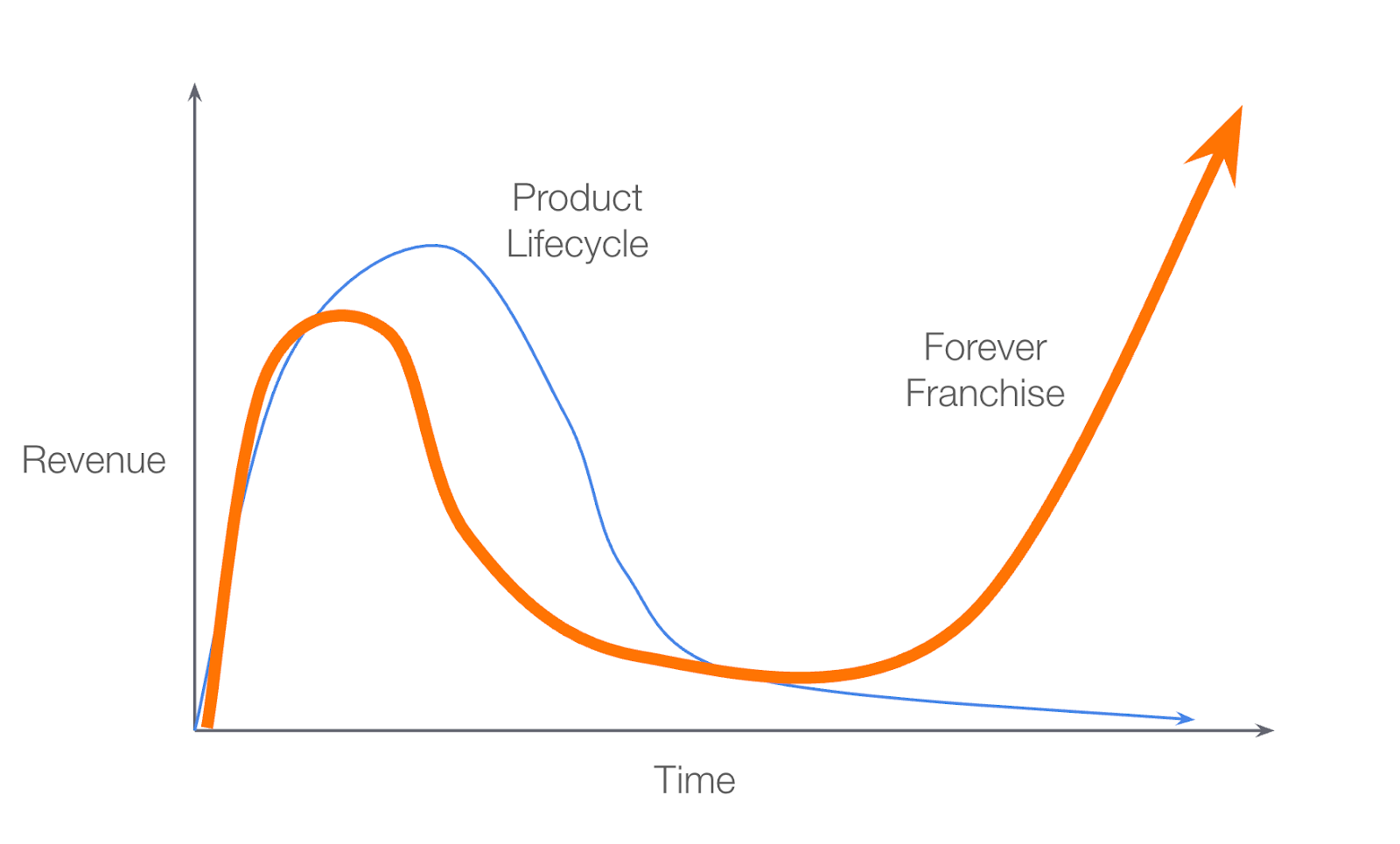

There is a second and even more frequently misread variant.

In this case, a game launches strong and appears successful, only to see its player base decline sharply soon after. Under the Product Lifecycle model, this pattern is treated as definitive failure. Player counts are compared to the launch peak, the narrative turns negative, and observers inside and outside the developer write the game off for dead.

This judgment is often reinforced by social, emotional, and organizational pressure. When metrics move against expectations and the broader consensus declares a game “dead,” even experienced operators and investors can lose conviction. The post-launch peak becomes an anchor, and deviation from it is treated not as a problem to be solved, but as evidence that the opportunity is gone.

Often that conclusion is wrong. If the underlying systems are flawed but fixable, and the development team corrects them, a game can recover and grow into a Forever Franchise, often becoming far larger than it ever was at launch.

No Man’s Sky is a dramatic example. It launched amid extraordinary hype, failed to meet expectations, and collapsed shortly thereafter. By conventional metrics, it was dead. Instead of abandoning the game, the team rebuilt its systems over time. Today, it is a thriving, long-lived franchise, much more valuable than it was at its initial peak.

Other examples abound. Apex Legends followed a similar growth trajectory after its early surge-and-drop, as did Pokemon Go and MapleStory Mobile. In these cases, many analysts interpreted the revenue declines as terminal decay rather than signals to reinvest, rebalance, and rebuild.

The mistake is treating the launch peak as the benchmark. In retention-driven businesses, that peak often marks the beginning of the real work, not the end.

It is easy to mistake this argument for a call for blind patience. It is not. The Forever Franchise model does not excuse poor execution or justify indefinite decline; it replaces the wrong yardstick with the right one. Under a retention-driven model, the standards become more demanding, not less: gameplay system health must improve, and player trust must be earned back. Patience without evidence is value destruction, but impatience under the wrong mental model is worse.

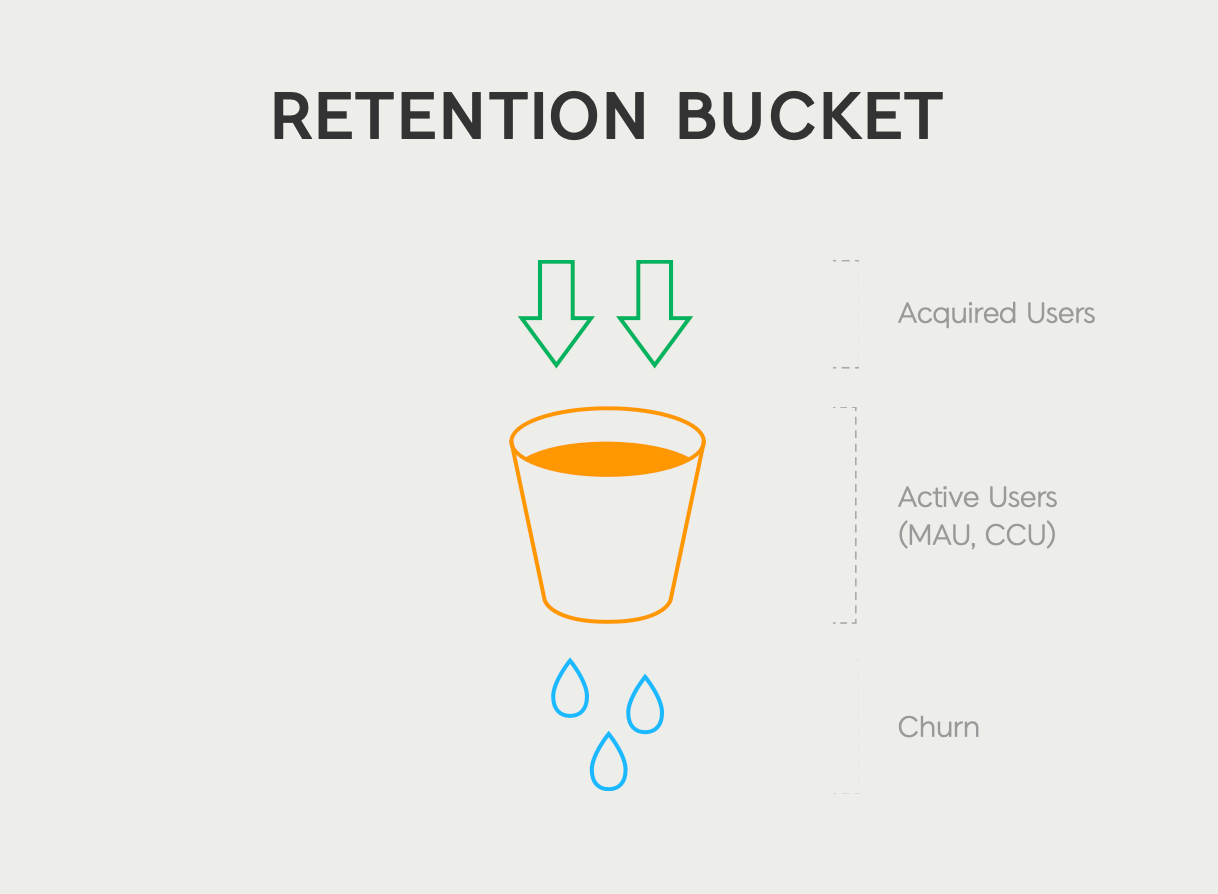

Developers who internalize the mental model of a Forever Franchise quickly get to work obsessing about how they will keep those players. The retention bucket — sometimes called the retention funnel — is the mental model that makes that obsession concrete.

Like all valuable mental models, it’s both easy to understand and powerful. Think of your user base as existing in a leaky bucket. You put water in the top (acquire users), and some always leak out the bottom (churn).

When you think of the world this way, you start obsessing about a very different set of drivers than someone who thinks their game will have a limited life:

While retention is often described mechanically as a “leaky bucket,” the reality is psychological, about earning player investment: players stay when they believe their time, effort, and identity invested in the game will continue to pay off.

Two very different business logics produce two very different outcomes:

As one small illustration of the different mindset, shortly after I joined Nexon in 2010, I congratulated the head of a development studio after he led a very successful new game launch. He shrugged, and responded: “Thanks, I guess. Come back and talk to me in a year and by then maybe I can relax.” His modesty reflected his deep understanding that the drivers of a Forever Franchise would take a lot longer to prove out.

None of this is easy. Several forces work against wholly adopting the Forever Franchise model, especially for teams shaped by the traditional games business:

Operators who overcome these forces think differently at every level. Retention comes before revenue, not because revenue doesn't matter, but because losing the player makes every monetization decision irrelevant. High retention gives you time: to build systems that earn player commitment, to iterate, and to monetize at the pace of player enthusiasm rather than management anxiety. It forces an obsession with the things that actually keep players: gameplay, content cadence, balance, server stability.

Smart long-term operators replace short-term optimization. You become willing to forgo near-term sugar highs in exchange for durable system health, resisting monetization choices that damage player trust. The hardest part of building a Forever Franchise is not spending more, but resisting the instinct to spend on the wrong things.

Organizationally, this requires treating a game as three distinct efforts, not one: New Game Development, Live Game Development, and Live Game Operations. Each is essential, and each demands different skills, incentives, and leadership.

To anyone who has built or operated a successful online game, these points are obvious. But a long-term, retention-first orientation remains depressingly rare, even today.

Once you understand what actually drives outcomes, the industry’s spending patterns start to look highly irrational. In baseball, getting on base was undervalued, so teams overpaid for visible statistics like RBIs. In games, the industry continues to overpay for legible inputs like graphics, production scale, and launch marketing spectacle. Durable live-service advantage rarely comes from those investments. It comes from system design, iteration, and judgment: capabilities that don’t scale with budget, cannot be bought easily, and compound enormously over time.

The opportunity to arbitrage Forever Franchises has existed globally for more than two decades. Why have so few exploited it? Understanding that the Forever Franchise model exists is no longer rare. Knowing how to act on it under pressure is. It requires rejecting the social proof of prevailing industry consensus, something most investors and management teams are structurally unable to endure.

Retention-driven businesses often look worst precisely when they are healthiest: revenue dips in the short term to rebuild systems, margins compress while operators engineer long-term compounding. Public-market investors are benchmarked quarterly, and boards reward visible near term revenue growth over invisible system health. Even investors who intellectually grasp the model often lack the mandate, governance, or emotional resilience to hold through periods when the numbers look bad but non-consensus fundamentals are improving. This is why the mispricing persists. The secret is out in the open, but the path is lonely, and it reliably attracts deep skepticism long before it delivers results.

Large swaths of investors still treat games as wasting assets, assuming revenue must decay over time. That assumption causes them to reliably mis-price assets:

Durable franchises often look inevitable in hindsight. In practice they are the product of deliberate choices: teams that believe longevity is possible and organize their technology, tools, and incentives around sustaining it. This phenomenon is not unique to games; the same pattern appears across media industries. In music, most profits historically came from the back catalog, even though charts and media attention focus almost entirely on new releases. Disney’s “windowing” strategy under Michael Eisner created multiple economic lives for the same films: theatrical, home video, television, and beyond.

The arbitrage has been hiding in plain sight for two decades. The mental models to exploit it are available to anyone willing to apply them. What has always been scarce is not the insight but the conviction to act on it.

Most people reason from mental models inherited from past success, even after the conditions that made them effective have changed. When those models stop working, it feels safer to defend them than to replace them. Going against the crowd is difficult not because the evidence is unclear, but because it threatens both identity and status.

In its pursuit of live service games, the industry’s constraint has not been capital or talent. It has collectively spent many billions on live-service development and M&A over the past decade, yet most of the largest publishers have struggled to produce durable, growing franchises. The problem was the mental model used to deploy those resources.

The Forever Franchise is not a new idea. The evidence has been visible for more than two decades. What has always been rare is the willingness to act on it under pressure: when the quarterly numbers look bad, when the consensus has turned negative, when the development team is asking for more time while the CFO needs revenue this quarter. That is precisely when it matters most.

For operators, the question is whether you can hold a retention-first orientation when every organizational instinct and every short-term incentive is pushing you toward extraction. For investors, the question is whether you have the mandate, the patience, and the conviction to be contrarian in both directions: selling into apparent strength when the underlying player base is eroding, and buying into apparent weakness when the market has mistaken a temporary revenue dip for terminal decline.

Most can't. That's why it’s an opportunity.